In recent years, the landscape of venture capital investment in innovative medicine in China has experienced a notable shift. Following a period of prosperity during the COVID-19 pandemic, Chinese VC funding peaked in 2021. But this has been followed by a substantial decline, caused by geopolitical tensions, the shift away from COVID research, and unsatisfactory returns from prior development programs.

Amidst this downturn, however, cell therapy has emerged as a beacon of opportunity for 2024 and beyond. And international pharmaceutical companies and their suppliers – including providers of instruments, cell lines, and high-end consumables – face a great opportunity to explore strategic partnerships to expedite clinical trials in the field.

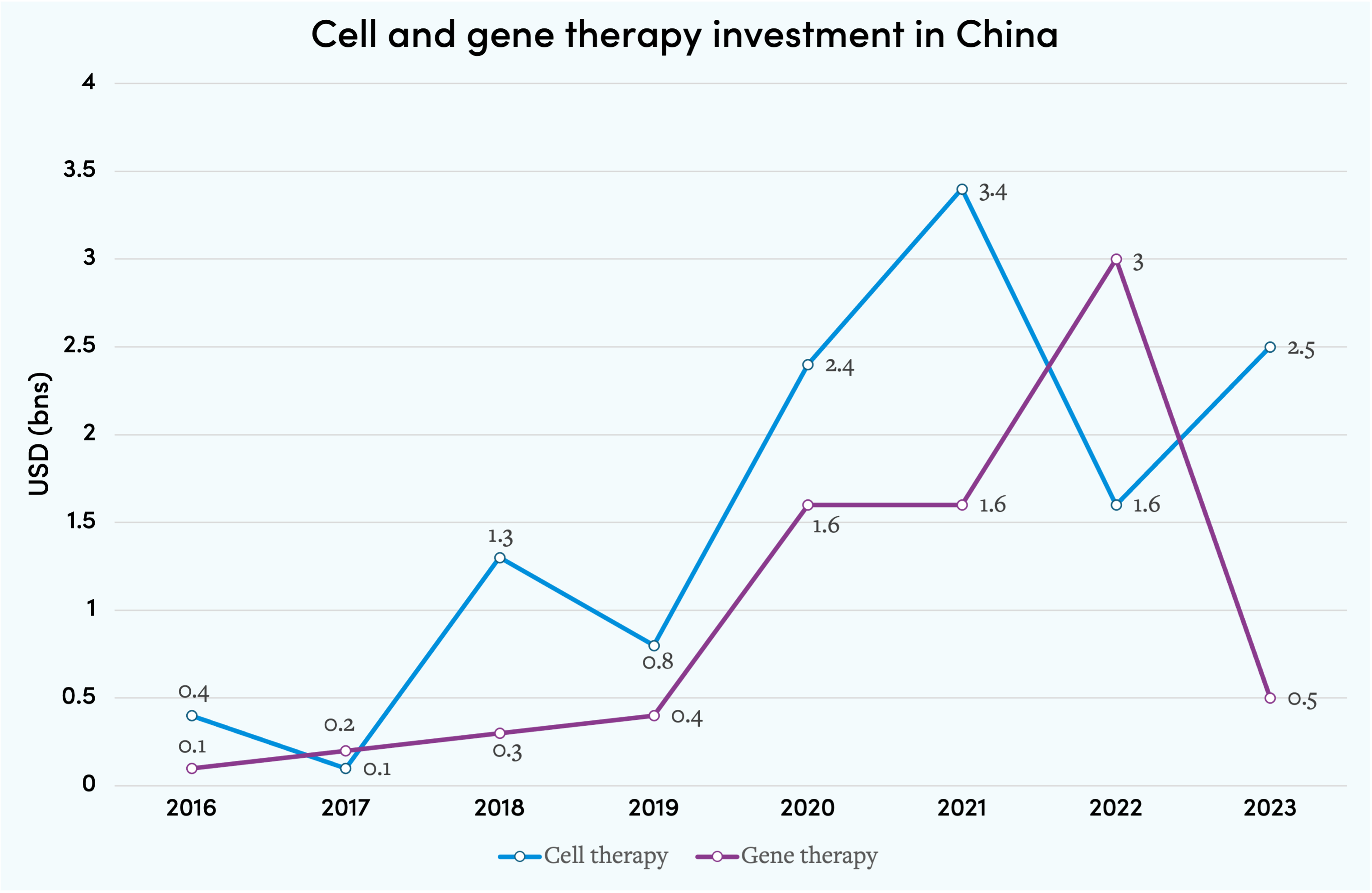

Changing investment dynamics

Investment in innovative medicine in China overall has recently been going through a cooling phase, with a marked decline in venture capital funding over the last two years.

The gene therapy sector, in particular, saw a striking 83% decrease in investment from 2022 to 2023, attributed to slow clinical progress and tightened gene editing supervision by China’s National Medical Products Administration (NMPA).

But China’s cell therapy ecosystem presents a very different picture – as the graph below clearly shows.

Increasing focus on – and government backing for – innovative medicine catalyzed a remarkable 51% post-COVID rebound in cell therapy funding in 2023, with investment reaching $2.5 billion.

And more than 2,000 cell therapy clinical trials – accounting for one out of three trials globally – are being conducted by Chinese players, underlining the country's growing influence in the global market.

CAR-T innovation

China's focus on cell therapy is particularly strong in the realm of Chimeric Antigen Receptor T-cell (CAR-T) therapy.

Among 2,034 cell therapy-related trials, 1,164 are focused on CAR-T. And, amongst these, 11 products have entered pivotal stages and two have filed New Drug Applications (NDAs) with the NMPA.

Four CAR-T drugs – developed by Fosun Kite, JW Therapeutics, IASO Biotherapeutics and Juventas – have already gained NMPA approval as of this January.

And the average price of $153,000 for Chinese CAR-T therapy is significantly lower than its US equivalent, creating a clear competitive advantage for Chinese offerings.

Supportive regulatory environment

China’s NMPA has also played a crucial role in fostering the remarkable growth of cell therapy in the country.

In 2022 alone, the NMPA published eight regulations to expedite the clinical progress of cell therapy drug development, demonstrating the government's commitment to these products.

Major Chinese cities – including Shanghai, Beijing, Tianjin, Shenzhen and Haikou – have also formulated local incentive plans for innovative cell therapy drugs. Including funding, clinical resources and accelerator support, these incentives are further facilitating a conducive environment for the sector’s expansion.

Entrants from Southeast Asia

Given this remarkable growth, China's cell therapy market is unsurprisingly capturing substantial overseas attention and emerging as an important target for new entrants.

Southeast Asian cell therapy players – most notably exemplified by Singaporean biotech company Lion TCR – have been particularly active in China.

Despite meeting initial challenges in the market, Lion TCR secured a $40 million investment from the Chinese government last year, highlighting the market's appeal to innovators and helping to drive the progress of clinical trials.

Global collaborations

There’s also considerable scope for international players to collaborate with Chinese firms to drive sales in their home markets.

Legend Biotech, for example, is a specialist in CAR-T, TCR-T and NK-based therapies which spun out from Nanjing GenScript Biotech in 2020. The company’s success with Carvykti – the first Chinese-developed cell therapy drug commercialized in the US – generated $500 million in sales for its collaborator, Johnson & Johnson, in 2023.

This has spurred other Chinese cell therapy startups – such as Juventas and CARsgen – to explore partnerships with international corporations.

Chinese firms are particularly seeking imported consumables and instruments – including iPSC differentiation, retro-viral gene transfer and cell cryopreservation technologies – to expedite product commercialization.

And, as more Chinese companies target overseas markets, opportunities for international suppliers to work with them on drug development will only increase.

Market entry approaches

Cell therapy in China, then, is an attractive, fast-growing market. But what approach should international companies take?

The answer varies according to the line of business you’re in. Cell therapy drug developers should seek links with Chinese contract development and manufacturing organizations (CDMOs) and contract research organisations (CROs) to support clinical trials.

They should work with these Chinese partners on investigator-initiated trials (IITs) to expedite data collection for global development. They should also engage large Chinese pharmaceutical companies to explore therapy technology licensing opportunities.

Cell line developers, meanwhile, should focus on engaging Chinese cell therapy developers to explore licensing opportunities.

And developers of instruments and consumables should seek suitable distribution partners as part of a regional strategy to maximise their customer reach.

Whatever your business focus, I also strongly recommend regular participation in cell therapy conferences to stay up to date on market trends and opportunities.

Brimming with opportunity

So, despite a downturn in China’s overall medical market and on-going geopolitical tensions, the country’s cell therapy landscape is resilient and brimming with opportunity.

With the government providing a supportive regulatory environment and growing interest from global players, the sector is poised for continued growth and offers international companies significant scope for successful partnerships.

To discuss your prospects in the Chinese medical market, you can reach Jake Li at jake.li@intralinkgroup.com